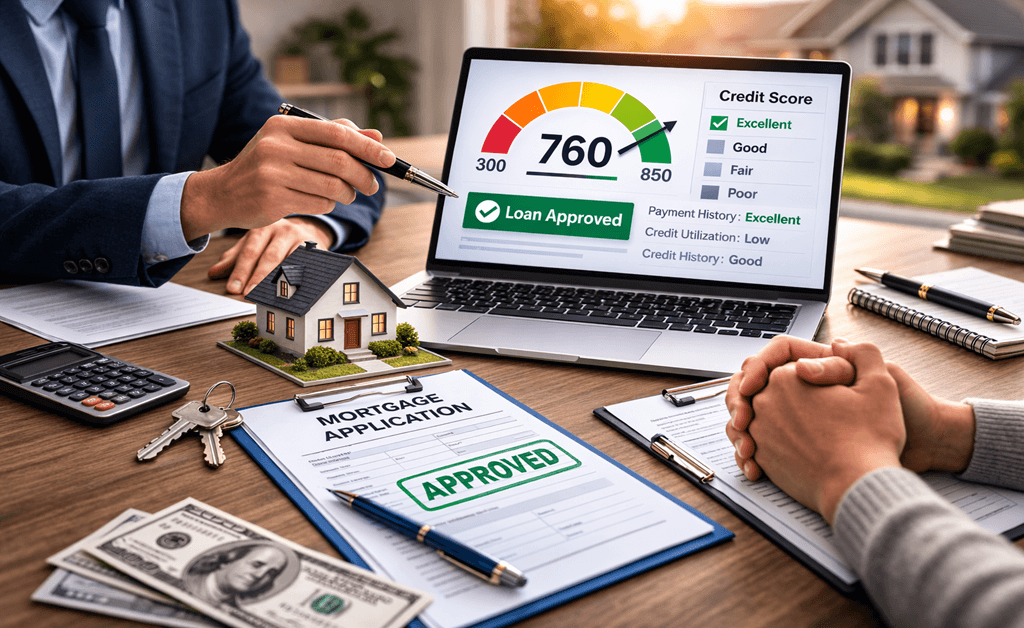

This is what we witness on a regular basis. A client comes to us with confidence and is ready to purchase a home because they have been shown a credit score of 760 through their mobile banking application. They have worked hard to save money for the down payment as well as manage their debt. But when we request their credit report to get them pre-approved for the purchase of the home, the credit score comes out to be substantially lower.

The discrepancy is there because the credit score you are viewing from a free app is never going to be the same score we use when determining whether or not you qualify for a loan. As mortgage experts at BrickWood Mortgage, we would like to eliminate some of this confusion so you know exactly what you are getting into when entering into the market of purchasing a home. So, what is my mortgage credit score?

Understanding the Three Major Bureaus

Before we examine some of the scoring models, it would be useful to know how and where your data comes from. In the United States, there are three companies that keep your financial history: Equifax, Experian, and TransUnion.

When you apply for a mortgage, we often do not review the credit score from just one of these sources. What we use is called a tri-merge credit report. This will take information from all three credit bureaus and provide us with a complete and comprehensive view of your creditworthiness. Because lenders may report to one credit bureau and not the others, or report at different times of the month, you may have a different credit score with each of the three credit bureaus. Which credit score do lenders use for home loans? This is something we can help with as a leading mortgage broker.

The Particular FICO Versions Used by Lenders

It’s here that the technical aspects come into play. Most personal credit monitoring services will display either a VantageScore or a FICO 8 score. These are great for personal financial tracking, but they aren’t the industry standard for residential lending.

The vast majority of residential mortgage lenders are obligated to utilize “classic” FICO scores to abide by the criteria established by Fannie Mae and Freddie Mac. In particular, we examine three different varieties. FICO Score 2 is provided by Experian, FICO Score 5 is provided by Equifax, and FICO Score 4 is provided by TransUnion.

Once we have these three scores, we usually calculate using the middle one to arrive at your interest rates and eligibility. Suppose you have scores of 720, 740, and 750. In that case, we may calculate using the 740 score. However, if you are applying for a joint mortgage, we calculate using the middle scores of both of you and then use the lower one to make a final decision.

Finding and Enhancing Your Mortgage Score

The reason why you might not be able to get your hands on free copies of these particular versions of FICO is that they are old models, and they might be very expensive to access through services like MyFICO in order to get your actual scores. But you can monitor your generic FICO 8 score.

If you find that your scores are not where you want them to be, there are things you can do to try to raise them. We always recommend to our clients that you pay down those high balances on your credit cards, as your utilization rate is a large component of these calculations.

In addition, you must make sure you’re not missing any payments, as payment history is the most important factor in calculating your scores. Last, you should not be applying for new credit cards or auto loans in the year prior to applying for your mortgage. Since these types of inquiries will lower your score, you want to be getting the lowest rate of interest possible. A credit score for mortgages can impact your ability to qualify and the rates offered.

Let Us Help You Through This Process

The difference between what you see on your app and what your lender sees may be frustrating, but it doesn’t have to be an obstacle to achieving your goal of homeownership. Knowledge is your greatest tool in this situation. At BrickWood Mortgage, we are committed to helping you understand your credit report and finding the right loan program for your individual circumstances. If you’d like more information about current mortgage interest rates in South Carolina, we are here to help!